Can FTX tokenize its own bankruptcy?

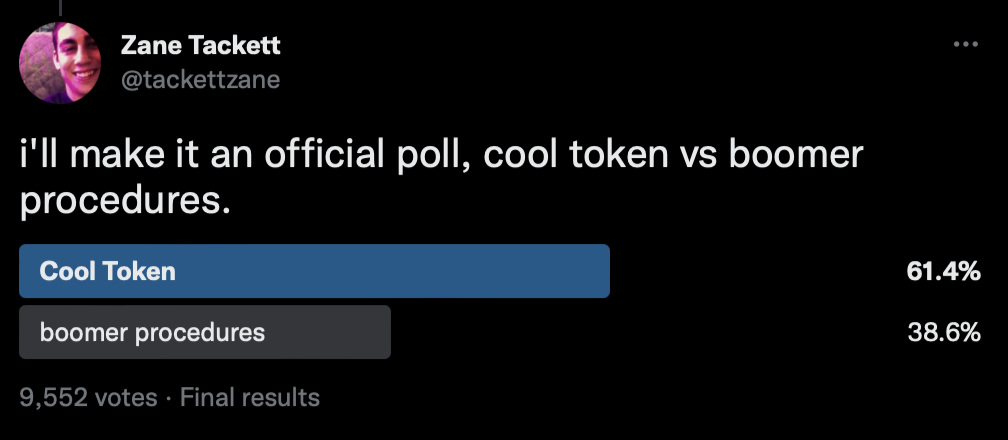

A former FTX employee, Zane Tackett, put out a Twitter thread a few days ago ending with a pointed — if biased — question: Should FTX issue a “Cool Token” or go through a traditional bankruptcy proceeding?

The poll clearly suggested that most people in the cryptocurrency industry felt a “Cool Token” was the way to go.

So, could FTX tokenize its debt and make customers whole?

It’s happened before

It’s impossible to speak about a tokenized debt offering without bringing up Bitfinex.

In 2016, Bitfinex was hacked for 119,000 bitcoins and gave almost all of its customers (Coinbase excluded) a haircut. However, this haircut wasn’t a simple “we took 36% of your assets on the exchange, move along.”

Everyone was given the BFX token on a one token for $1 worth of funds basis. Next, a Recovery Rights Token (RTT) was established to push traders to move the BFX token into what was, more or less, Bitfinex equity (they did this due to the fact that they’d lost their Taiwanese banking partner and had little-to-no cash on hand). There’s still even a website explaining it within the Bitfinex ToS.

This BFX token was moved through a special purpose vehicle (SPV) via BnkToTheFuture and Simon Dixon and many individuals still have Bitfinex equity to this day.

Meanwhile, with the arrest of Ilya Lichtenstein and Heather Morgan, it seems as if the BFX token, RRT token, and Bitfinex equity have proven to be a boon for victims of the hack.

A day late, $10 billion short

While the hack at Bitfinex negated 36% of customer funds, the unfortunate reality at FTX appears to be that, well… there are few, if any, liquid customer funds remaining. Not only this, but the extremely complex corporate structure and the initiation of bankruptcy proceedings for all 100+ companies pretty much ensures a tokenized debt offering is dead in the water.

Protos was able to speak with an attorney who has an understanding of the ongoing issues with FTX and Alameda.

The lawyer explained that there are tiered levels of complexity when it comes to bankruptcy proceedings and that FTX “goes beyond the most complex cases — it’s a catastrophic event,” (our emphasis).

As to the legality? For Bitfinex, the attorney stated, “they were stolen from and facing a hole. They did a fundraising mechanism to fill that hole and it managed to tide them over.” But FTX and Sam Bankman-Fried face a much steeper uphill battle.

“Imagine he says we’re going to do a coin issuance, assuming it’s somehow not a security… he might as well do a GoFundMe instead. Once he’s moved into bankruptcy court, he’d need to get a sign-off from the court to issue any kind of token. He can’t change jurisdictions, can’t alter the name, and can’t alter the company structure during bankruptcy. There’s no reason to issue a token.”

Read more: We searched for FTX’s ether — and we have questions

Tokenized debt dead in the water

While the majority of industry respondents to Zane Tackett’s tweet seem to be on board with a “Cool Token” for the total insolvency of FTX and its subsidiaries, the reality is it isn’t just unlikely, it’s near impossible.

For what it’s worth, it appears someone more familiar with issuing tokenized debt seems to agree. Phil Potter, the former CSO for Bitfinex and Tether responded clearly and matter of factly to the suggestion: “In principle, a ‘roll your own restructuring’ via some sort of token model is WAY preferable to bankruptcy court, but only if your token model would effectively mimic what would otherwise be a likely outcome in court — Bitfinex was quite simple compared to FTX/Alameda.”

Oh, and it’s worth mentioning that bankruptcy won’t protect Sam and the other executives from a slew of incoming civil and, probably, criminal court cases on the horizon.

For more informed news, follow us on Twitter and Google News or listen to our investigative podcast Innovated: Blockchain City.