Michael Saylor says bitcoin credit now has a yield curve — thanks to him

On Monday, Michael Saylor announced the IPO of his fourth series of preferred shares offering perpetual yield, Stretch (STRC).

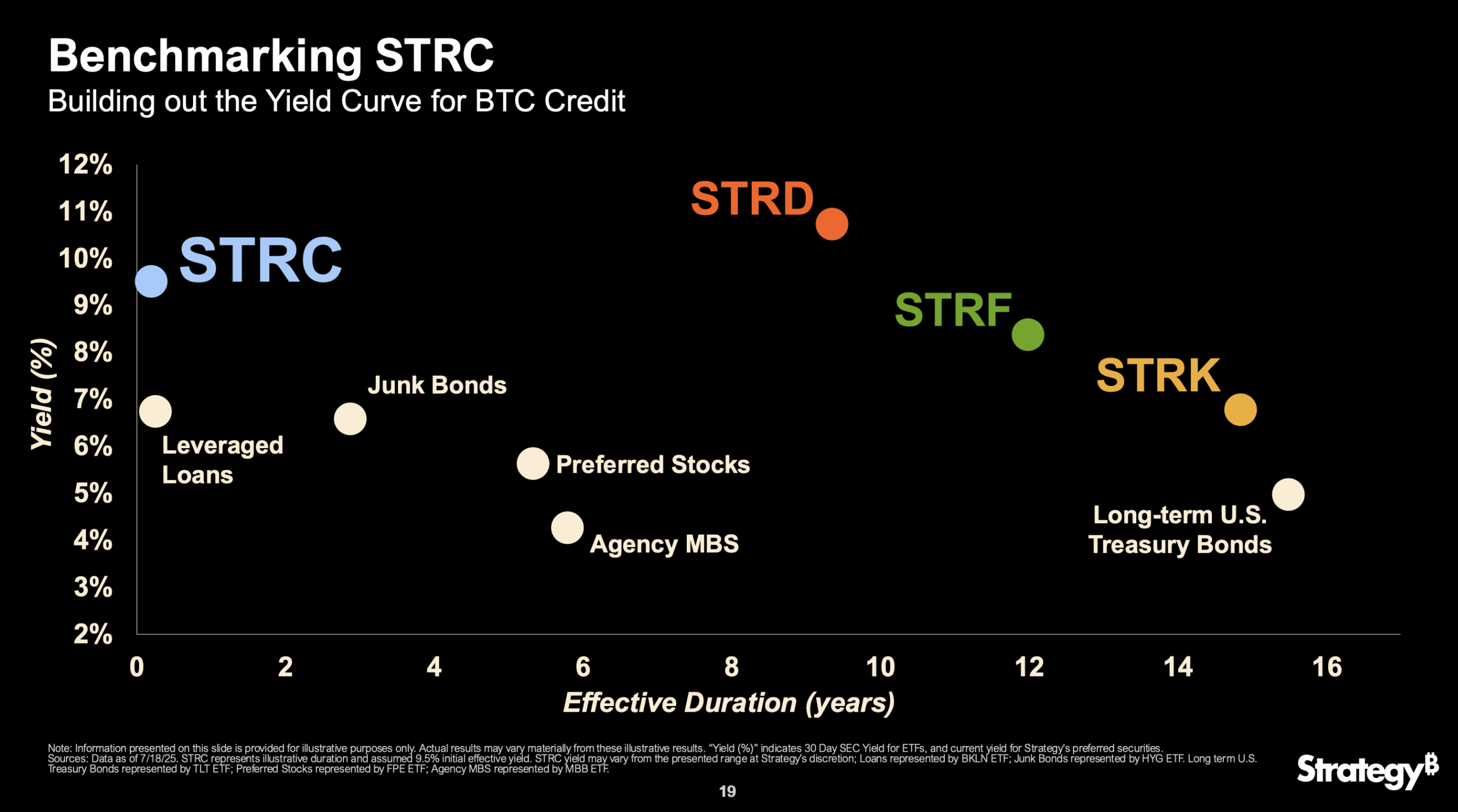

With its debut, Saylor claims that he’s “building out the yield curve for BTC credit” and has published the world’s first curvature of bitcoin (BTC) credit for the world to behold.

As founder of the world’s largest publicly traded BTC treasury company, Saylor is unique in his ability to issue yield-bearing securities while holding over 3% of the circulating supply of BTC.

This privilege, according to Saylor, allows his company to benchmark its rates against the yield curve of multi-trillion dollar bond markets like agency mortgage-backed securities, junk bonds, and even US Treasuries.

Indeed, according to a diagram published yesterday alongside the STRC IPO announcement, the supposed BTC credit yield that MicroStrategy is building resembles the yield curve of these massive instruments plus a slight premium due to MicroStrategy’s idiosyncratic risks.

Specifically, according to Saylor, investors are pricing Strife (STRF) — another of MicroStrategy’s dividend-yielding preferred shares — at a “340 basis point credit spread above the 20-year Treasury bond.”

In other words, for just an extra 3.4% yield, investors are allegedly willing to forego the full faith and credit of the US government for one of MicroStrategy’s preferreds.

Read more: We made a dictionary of MicroStrategy’s invented terminology

Bitcoin doesn’t have a yield curve

An actual credit yield curve is a graph of yield percentages (interest rates, displayed as percentages) and the maturity lengths of bonds with similar credit quality.

For most series of government or high-grade corporate bonds, yields curve upward.

A positive, up-and-to-the-right slope is normal. Longer-duration bonds yield more than shorter-term bonds because investors demand additional compensation for greater uncertainty tied to time.

According to Saylor, MicroStrategy’s BTC credit yield curve is slightly inverted — down and to the right — because it reflects the reality of yields available in today’s market.

Short-term junk bonds and leveraged loans, on the other hand, offer average yields of 6-7% percent today, while long-term US Treasuries offer yields of just 4.9%.

Of course, the problem with Saylor’s so-called yield curve is that it graphs the yields of different instruments. A yield curve should have a positive slope in normal market conditions because the only variable that changes is time — not time plus the instrument itself.

In addition, Saylor’s yield curve doesn’t graph bond yields at all. Instead, it graphs dividend rates from preferred shares that are junior to actual bonds in seniority.

Saylor conveniently excluded the actual bond yields that MicroStrategy has issued from his supposed BTC credit graph.

Moreover, MicroStrategy’s yield curve is not the yield curve of BTC credit at all. In fact, BTC has no yield, nor does BTC offer any form of credit.

BTC is simply an asset that transacts on a blockchain. Calling four preferred shares of a company “the yield curve for BTC credit” is aspirational and confusing.

On the capital stack, STRC is senior to Stride, Strike and MicroStrategy (MSTR) common stock. It’s junior to Strife and the company’s debt, including six series of convertible notes.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.